Download Kansas K 30 Form

Download Kansas K 30 Form

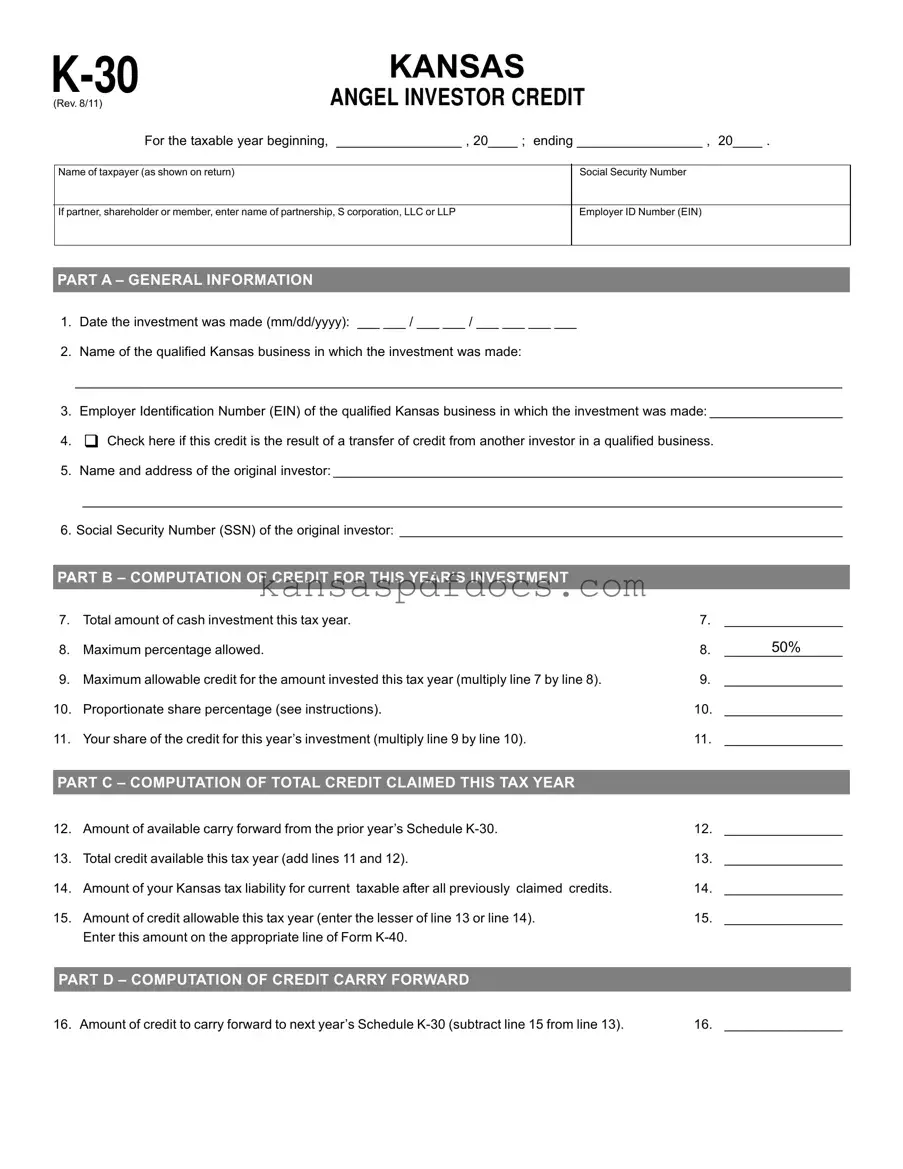

The Kansas K-30 form is a crucial document for individuals seeking to claim tax credits as angel investors in qualified Kansas businesses. This form facilitates the process of reporting cash investments made during the taxable year, allowing investors to benefit from a tax credit of up to 50% of their investment. The K-30 form requires detailed information, including the taxpayer's name, Social Security number, and specifics about the qualified business receiving the investment. It comprises several sections, starting with general information about the investment and the business, followed by computations to determine the allowable credit for the current tax year. Investors must also calculate any carry-forward credits from previous years, ensuring they maximize their benefits. Furthermore, the form includes provisions for transferring credits between investors, enhancing flexibility in tax planning. Understanding and accurately completing the K-30 form is essential for investors to effectively navigate the tax implications of their contributions to Kansas's economic growth.

The Kansas K-30 form is a crucial document for individuals looking to claim tax credits for investments made in qualified Kansas businesses. However, it is often accompanied by several other forms and documents that help streamline the process and ensure compliance with state regulations. Below is a list of related documents that may be required when filing the K-30.

Understanding these documents and their purposes can help investors navigate the tax credit process more effectively. Proper documentation not only ensures compliance but also maximizes the potential benefits of the angel investor tax credit in Kansas.

Misconceptions about the Kansas K-30 form can lead to confusion and frustration for taxpayers. Here are five common misunderstandings, along with clarifications to help ensure accurate filing.

This form is designed for individual investors, including those who are part of small businesses or partnerships. Anyone who qualifies as an angel investor can utilize this form to claim tax credits for their investments in qualified Kansas businesses.

Not all investments are eligible. The investment must be made in a business that has been approved by the Kansas Technology Enterprise Corporation (KTEC) as a qualified business. It is essential to verify the business's status before making an investment.

The maximum allowable credit is capped at 50% of the cash investment made during the tax year, subject to specific limits. For instance, no investor can claim more than $50,000 for a single Kansas business or $250,000 in total tax credits for the year.

While it is true that unused credits can be carried forward, they cannot be claimed indefinitely. Investors must use the credits within a certain timeframe, and specific rules apply to how long they can be carried forward.

Proper documentation is crucial. Taxpayers must keep a copy of the approved KTEC certification form and any relevant transfer documentation if credits are transferred from another investor. The Kansas Department of Revenue may request this information, so maintaining accurate records is essential.

When filling out the Kansas K-30 form, ensure that all personal and business information is accurate. This includes your name, Social Security Number, and the details of the qualified Kansas business where the investment was made.

The investment must be made in a business approved by the Kansas Technology Enterprise Corporation (KTEC). Verify the business's status before proceeding with your investment.

Be mindful of the maximum credit limits. For individual investors, the maximum credit is 50% of the cash investment, with a cap of $50,000 for a single Kansas business and $250,000 per year for individual investors.

When calculating your credit, keep in mind that you must multiply the total cash investment by the maximum percentage allowed. This will help you determine the maximum allowable credit for the current tax year.

If you have carry-forward credits from previous years, include these amounts in your calculations. This can significantly affect the total credit available to you for the current tax year.

Finally, remember that documentation is crucial. Keep a copy of the approved KTEC certification and any other relevant documents for your records. This is important in case the Kansas Department of Revenue requests additional information.

Handicap Placard Kansas - Renewals help maintain the integrity of the disabled parking program in Kansas.

In addition to establishing the operational framework of your LLC, having a well-drafted Operating Agreement can significantly reduce the risk of disputes among members. It ensures clarity in roles and responsibilities, which is essential for the smooth functioning of the business. To help you create this important document, you can access a valuable resource at https://newyorkform.com/free-operating-agreement-template, where you'll find a free template that guides you through the necessary components of an effective agreement.

Tr 42 - The lien holder’s consent must be captured through notarization for the issuance of the title.

How to Start an Llc in Kansas - Be aware of the penalties for late filing to avoid unnecessary fees.