Download Kansas K 19 Form

Download Kansas K 19 Form

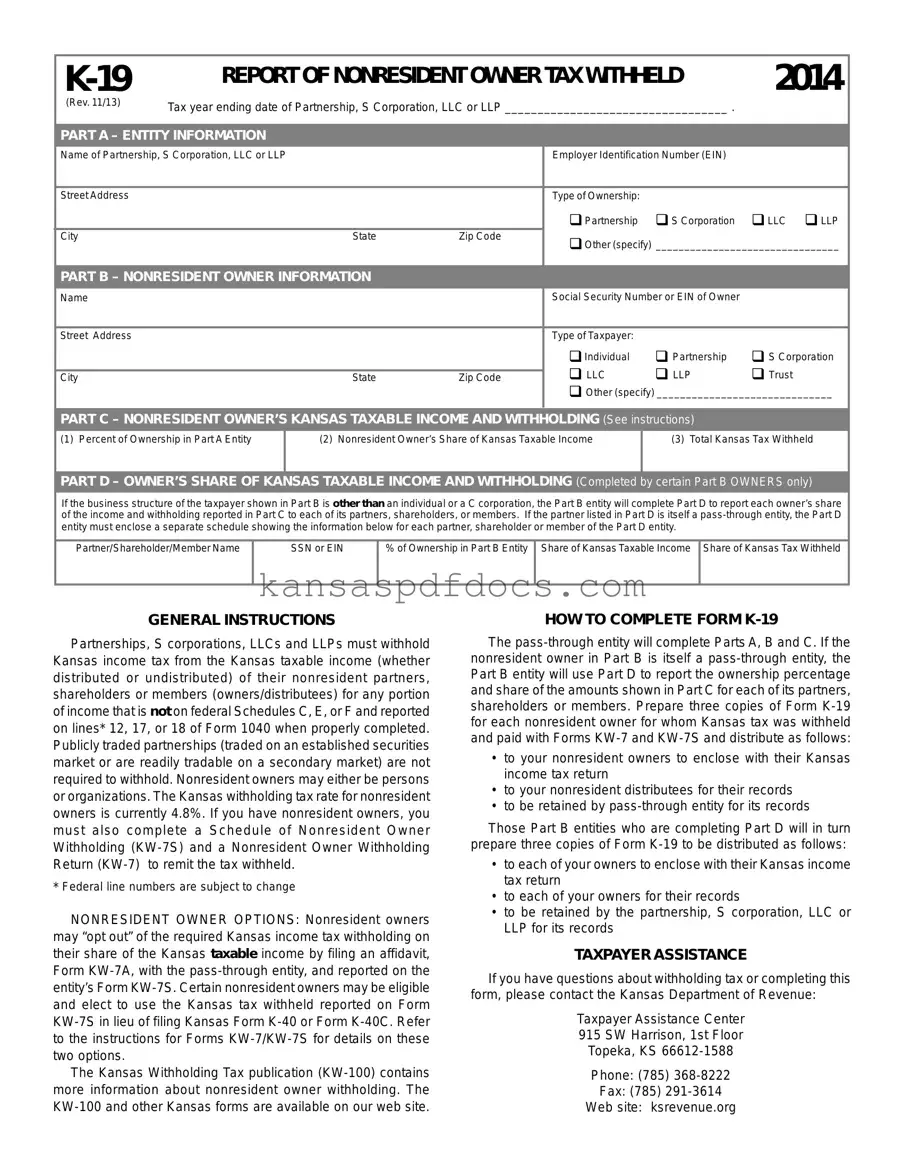

The Kansas K-19 form plays a crucial role in the state's tax system, particularly for partnerships, S corporations, limited liability companies (LLCs), and limited liability partnerships (LLPs) that have nonresident owners. This form is designed to report the Kansas income tax that must be withheld from the taxable income of these nonresident owners, whether that income is distributed or not. It includes several sections that gather essential information, such as the entity's details, the nonresident owner's information, and the specifics of the taxable income and withholding amounts. Notably, the form also outlines the process for reporting ownership shares and tax withheld for nonresident owners who are themselves pass-through entities. The withholding tax rate for nonresident owners is currently set at 4.9%, and entities must comply with additional requirements, including the completion of accompanying forms like the KW-7S and KW-7. For those who wish to opt out of withholding, the form provides an avenue through an affidavit. Understanding the K-19 form is vital for ensuring compliance with Kansas tax regulations and avoiding potential penalties.

The Kansas K-19 form is essential for reporting nonresident owner tax withholding for various business entities. Alongside this form, several other documents are commonly used to ensure compliance with Kansas tax regulations. Each of these forms serves a specific purpose and helps streamline the tax reporting process for both entities and their nonresident owners.

Understanding these forms and their purposes is crucial for compliance with Kansas tax laws. Proper completion and timely submission can prevent potential issues with tax authorities and ensure that both entities and nonresident owners fulfill their tax obligations accurately.

Understanding the Kansas K-19 form can be challenging, and misconceptions can lead to mistakes. Here are seven common misconceptions about the K-19 form, along with clarifications to help you navigate this important document.

By addressing these misconceptions, you can ensure a smoother process when dealing with the Kansas K-19 form. If you have further questions, consider reaching out to the Kansas Department of Revenue for assistance.

Understanding the Kansas K-19 form is crucial for compliance and accurate reporting. Here are key takeaways to keep in mind:

Timely and accurate completion of the K-19 form is essential to avoid penalties and ensure proper tax reporting.

Childcare Registry - Approval from medical professionals is key to validating the health assessments provided on the form.

Where to Get a Sellers Permit - Applicants must certify their good moral character and truthfulness of the application.

To ensure a clear and lawful transfer of ownership, utilizing resources like the NY Templates can be invaluable, as they provide a streamlined Mobile Home Bill of Sale form that captures all necessary information between the buyer and seller, thereby facilitating a smooth transaction.

New Hire Reporting Kansas - The K-BEN 3211 requires details about the claimant’s last day of work.